Score Simulator Credit Karma Style Tool

Model how everyday credit actions could shift your score and use the built-in accumulated interest calculator view to understand how credit changes affect borrowing cost.

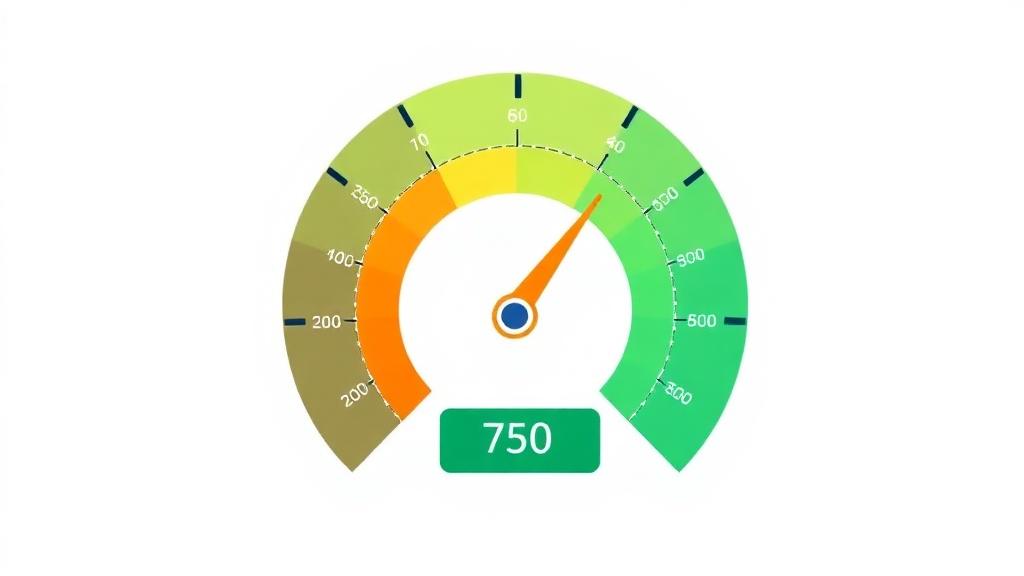

What This Simulator Does

A credit score simulator models how common credit actions could shift your score before you actually take them. Lower utilization tends to help, missed payments hurt sharply, opening new accounts dings the score temporarily, and paying off balances delivers a steady boost.

Because credit decisions affect borrowing cost, this tool also shows the yearly interest your projected APR would generate on a $5,000 balance, plus the compounded version — the figure that actually shows up on a credit card statement.

For more context on improving credit before applying for loans, read our blog and compare repayment costs with the equated monthly installment calculator.

How to Use It

Enter your current score and adjust the inputs to model common moves. The engine combines each input into a single projected score capped between 300 and 850. Try dropping utilization by 20 points, then add a single missed payment, then reset and pay off two cards — each scenario shows how the model weights different actions.

What Drives Your Score

Payment history and credit utilization are the heaviest factors, followed by length of history, credit mix and new inquiries. Missing one payment can cost up to 60 points; paying off cards can earn back 10 each.

Tied closely to your score is your borrowing cost. Use our EMI calculator to see how a higher score (and lower rate) cuts long-term interest on any loan.

Yearly vs Compounded Interest

The yearly figure shown above is the simple interest your APR would generate on a $5,000 balance. The compounded figure assumes monthly compounding — closer to how credit card issuers actually charge interest, and always larger than the simple number.

That gap is why financial planners insist you pay credit cards in full each month. For larger debts or longer horizons, model them with our compound interest calculator.

Habits That Build a Strong Score

Always pay on time, keep utilization under 30% (ideally under 10%), avoid opening multiple new accounts in short bursts, and let your oldest accounts age. Check your credit report at least yearly for errors and re-run the simulator every few months to track progress.

FAQs

Is this an official credit score?

No. It is an educational simulator. Real scores are calculated by FICO and VantageScore using full credit data.

Why does utilization matter so much?

Utilization is one of the largest weighted factors in any score model — dropping it can boost scores within a single billing cycle.

How long does a missed payment hurt?

Missed payments can stay on your report for up to 7 years, though impact lessens over time.

Will checking my score lower it?

No — soft inquiries (self-checks, prequalifications) do not affect your score.

What's the difference between simple and compounded interest here?

Simple interest is the flat yearly figure; compounded interest reflects monthly compounding, which is closer to how credit cards actually charge.